The Benefits of Critical Illness Insurance

Safeguarding Your Retirement: The Benefits of Critical Illness Insurance

Planning for retirement is a lifelong endeavor requiring careful consideration of various financial elements. One often-overlooked component of retirement planning is preparing for the unexpected: a critical illness such as cancer, stroke, heart attack, or countless other life-threatening conditions such as Parkinson’s, ALS, MS, loss of limbs, and organ transplants, to name a few.

You can save and plan all you want, but should a serious illness occur, it could throw even the best-laid plans off course, setting your retirement goals and dreams back by years.

In Canada, the incidence of these illnesses is still significant. In the event of such an occurrence, critical illness insurance is there to protect your savings and financial peace of mind. This article will delve into the benefits of critical illness insurance, shedding light on Canadian cancer, stroke, and heart attack statistics (the “big three” where we see the most claims), and how this coverage can play a pivotal role in securing your retirement dreams.

Understanding the Threat: Canadian Cancer, Stroke, and Heart Attack Statistics

Before delving into the benefits of critical illness insurance, it's crucial to grasp the magnitude of the health risks posed by cancer, stroke, and heart attacks in Canada.

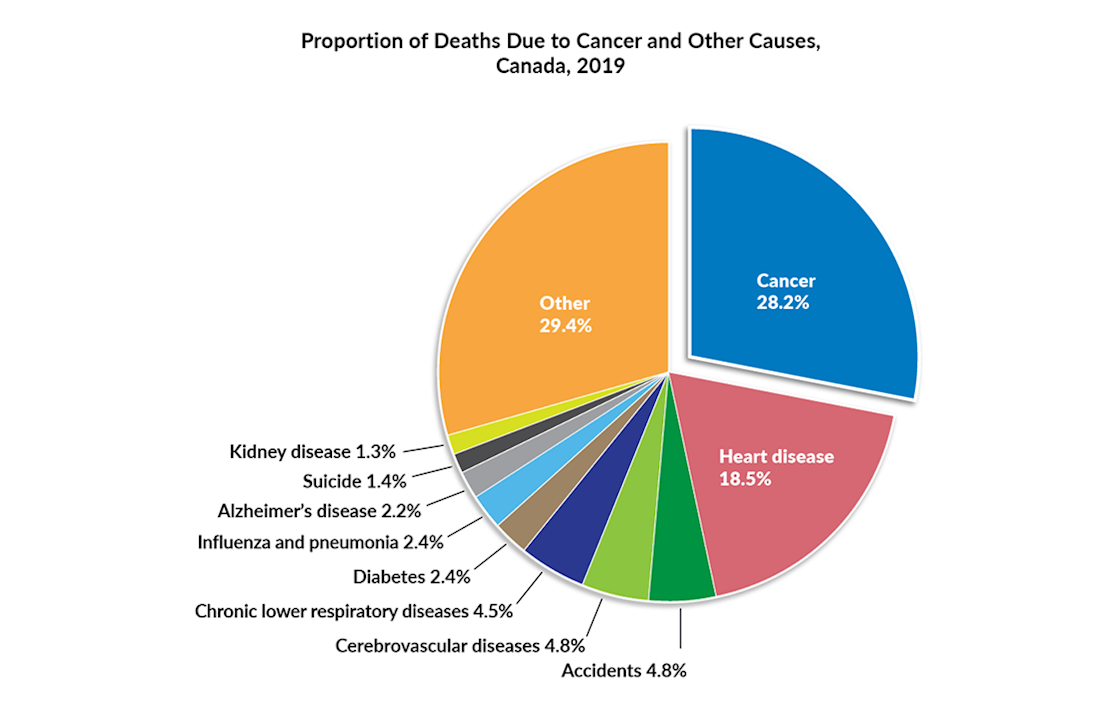

Cancer:

Canada has one of the highest cancer rates in the world. Researchers estimate 233,900 new cancer cases and 85,100 cancer deaths in Canada in 2022.1

Cancer is the leading cause of death in Canada and is responsible for 28.2% of all mortalities.1

The financial toll is immense, with cancer patients often incurring substantial medical expenses and lost income during treatment.

Stroke:

Strokes effect over 100,000 Canadians annually, or roughly 1 every 5 minutes.2

Stroke is the leading cause of hospitalizations, disability, and death in Canada.3

Survivors of strokes often require extended rehabilitation and may face long-term disability, impacting their ability to work and earn.

Heart Attack:

Over 60,000 heart attacks occur in Canada each year.4

Heart disease, including heart attacks, is the second leading cause of death, and the first cause of years of life lost (i.e. life expectancy).

Recovery from a heart attack may involve lifestyle changes and ongoing medical care, potentially impacting one's ability to continue working.

The Benefits of Critical Illness Insurance

Given the significant health risks posed by these illnesses, it is prudent to explore the benefits of Critical Illness (CI) Insurance, especially in the context of retirement planning.

What is CI?

Critical illness insurance provides a tax-free lump-sum payment typically 30 days after surviving a diagnosis, offering financial support when you need it most.

These tax-exempt funds can be used to cover medical expenses, mortgage payments, daily living costs, or any other financial obligations, ensuring that your retirement savings remain untouched.

Preservation of Retirement Savings:

Without critical illness insurance, a severe illness can deplete your retirement savings rapidly.

By receiving a lump-sum benefit, you can preserve your hard-earned retirement funds, preventing the need to dip into your nest egg prematurely.

Flexibility and Peace of Mind:

The funds from critical illness insurance are entirely flexible, allowing you to use them as needed. Whether it's to access innovative treatments, hire caregivers, or provide time off work for your spouse or family that may be providing you care, you have the autonomy to decide.

This flexibility provides peace of mind, knowing that your financial affairs are in order during a challenging time.

Coverage Beyond Traditional Health Insurance:

Critical illness insurance complements traditional health insurance by covering expenses that may not be reimbursed, such as experimental treatments, travel for specialized care, or modifications to your home for accessibility.

In many cases, an incidence of critical illness will often also result in a claim for Disability Insurance, however not everyone has Long-Term Disability Insurance. Furthermore, the wait period can often be up to 90-120 days and for a much smaller amount, really only providing income replacement or a slow drip that does not afford many extras aside from simply keeping you afloat. Critical Illness bridges the gap between immediately needed healthcare costs and personal financial resources.

Early Detection and Better Treatment Outcomes:

Many critical illness insurance policies offer additional services. For example, Teladoc Medical Experts® provides second opinions from world-renowned specialists and improves treatment plans. LifeWorksTM is another service that offers counseling services and legal and financial consultations.

These additional supports can improve your chances of early diagnosis and better outcomes, enhancing your overall health and longevity.

Planning Considerations with Critical Illness Insurance

1. Return of Premium Options

CI Insurance is quite unique in that it is the only insurance with a 100% Return of Premium (ROP) option rider. Two types exist; a full ROP on death or an ROP on Surrender or Expiry. You also have an option for both types, meaning that no matter the outcome, you will get back everything you invested into the policy completely tax-free. There are three different possibilities:

- You will not survive the required 30 days after diagnosis, in which case your family receives all the premiums you ever paid into the policy.

- You survive without making a claim, in which case you can surrender or allow the policy to naturally expire and receive back all of the premiums ever paid.

- The policy does what it is intended to do and pays you a lump sum amount if you become critically ill.

2. Not just for Adults

Critical illness insurance is often associated with adults, but it's equally important for children. Here's why:

Financial Protection for Families: When a child is diagnosed with a critical illness like cancer, the emotional toll on the family is immense, and the financial impact can be equally daunting. Medical bills, specialized treatments, and time away from work affect parents' ability to support their family and maintain their own financial stability.

Coverage for Childhood Ailments: Critical illness insurance for children typically covers a range of conditions, including congenital diseases and various pediatric illnesses. Having this coverage ensures that the family can focus on their child's recovery rather than worrying about financial burdens.

Future Insurability: Purchasing critical illness insurance for a child also secures their insurability for the future. In the unfortunate event that they develop a critical illness as adults, they are better able to obtain coverage, face fewer exclusions of covered conditions, and lower premiums. Nobody knows what the future may hold, but it is reasonable to believe that policies and medical definitions of today may be more inclusive than policies of the future. In the future it may be much harder to qualify for a claim.

Unique Plan Options and Future Gifts: Sun Life Financial has one of the more unique Child CI policies available in the marketplace, which may be purchased for a child to age 75 as early as 10 days old. The Return of Premium option differentiates the policy, where at the Child Age 25, providing there has been no claim, the parents will receive 75% of the premiums ever paid back to them tax-free. The remaining 25% that is unpaid remains in the policy and continues to accrue for the benefit of the child. At this age, many of our parent/grandparent clients choose to turn the policy over to the child.

3. Business Owners and Key Personnel

For business owners and key individuals within companies, critical illness insurance offers unique advantages:

Business Continuity: In a small or medium-sized business, the owner or key personnel often play a pivotal role in the company's success. If one of them were to fall critically ill, the business could face severe disruptions. Critical illness insurance can provide funds for temporary replacements, enabling business operations to continue smoothly during the owner's or key person's recovery.

Loan Protection: Many business owners have loans associated with their businesses. CI insurance can be structured to cover outstanding loans, ensuring that the burden of repayment doesn't fall on the business or their family during a challenging time.

Buy-Sell Agreements: In the case of business partnerships, a buy-sell agreement funded by critical illness insurance can ensure a smooth transition if one partner becomes critically ill or passes away. This agreement stipulates how the ownership will be transferred in such situations, protecting the interests of both the business and the individuals involved.

Unique Planning Opportunities: A concept sometimes employed with Corporately Owned CI is a Split Dollar or Shared Ownership Arrangement. In this strategy, the corporation owns a CI policy on the life of a shareholder (or key employee). The corporation pays the premium while the shareholder personally pays for the ROP cost. This approach effectively offers the best of both worlds, where the bulk of the insurance cost is owned tax favourably within the corporation and the tax-free nature of the ROP is owned and eventually collected tax-free by the stakeholder. Note: It is important to note that this strategy should be discussed with your tax preparer as CRA deem this policy to be a shareholder benefit. We are happy to consult with your Accountant to see if this approach might be worth considering.

Conclusion

In the pursuit of a successful retirement, critical illness insurance stands as a key planning pillar, shielding you and your loved ones from the financial devastation that can accompany a severe illness. By providing a tax-free lump sum upon diagnosis, critical illness insurance offers essential financial protection, preserving your retirement savings and ensuring you can focus on your health and recovery. Its flexibility and coverage beyond traditional health insurance make it a vital component of a comprehensive retirement plan. Moreover, early detection, second opinions, and expert treatment advice embedded in some policies contribute to better overall health outcomes.

Critical illness insurance is not limited by age or occupation. It is a versatile financial tool that can provide peace of mind and essential protection for children and serve as a strategic asset for business owners and key personnel. Whether you are a parent concerned about your child's well-being or a business leader safeguarding your company's future, critical illness insurance offers the security and flexibility needed to navigate life's unexpected challenges while securing a prosperous tomorrow.

If you have not yet had this conversation with your Innova Wealth Advisor and you’re looking for that kind of peace of mind, please contact us and ask about Critical Illness Insurance for you and your family members.

Build. Protect. Prosper -with, Innova Wealth.

Watch our explainer video here:

References

- Cancer Statistics at a Glace: https://cancer.ca/en/research/cancer-statistics/cancer-statistics-at-a-glance

- Heart & Stroke on the Rise: https://www.heartandstroke.ca/what-we-do/media-centre/news-releases/stroke-in-canada-is-on-the-rise

- TIA: https://static.cambridge.org/binary/version/id/urn:cambridge.org:id:binary:20230227143629583-0245:S0317167122003444:S0317167122003444_tab2.png

- Heart Disease in Canada: https://www.canada.ca/en/public-health/services/publications/diseases-conditions/heart-disease-canada.html

{kind=link}

- Hits: 10457