The Misconceptions of Dividend Investing

For many Canadian investors - particularly retirees - dividend investing can feel like an ideal strategy.

The concept is simple and appealing: build a portfolio of dividend-paying companies, collect steady income each month or quarter, and avoid having to sell investments to fund retirement spending.

And to be clear, we do think that dividends can play a role within a well-structured portfolio.

However, a common misconception is that dividends themselves automatically make an investment ‘better,’ ‘safer,’ or more effective at compounding wealth over time.

In our view, sophisticated portfolio construction tends to focus less on dividend yield alone, and more on diversification, capital preservation, tax efficiency, total return, and the ability to compound wealth consistently over time.

Dividends Are Not “Free Money”

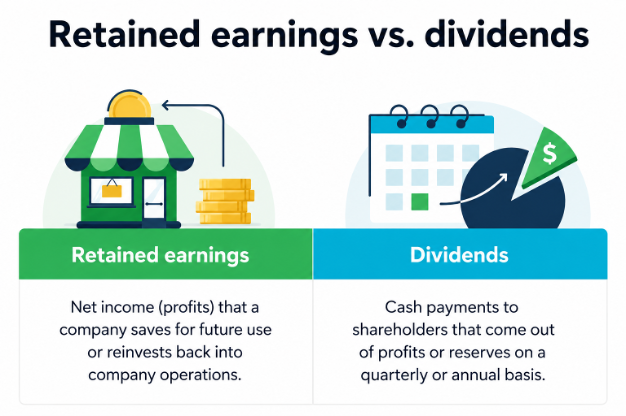

One of the most common misunderstandings surrounding dividend investing is the belief that dividends create additional return independent of the investment itself.

In reality, companies generally have two primary options with the profits they generate: distribute a portion back to shareholders through dividends, or retain those earnings within the business to support future growth initiatives.

Source: https://quickbooks.intuit.com/r/growing-a-business/calculate-retained-earnings/ (Aug 4th, 2025)

When a company pays a dividend, it is effectively transferring a portion of its value directly to shareholders rather than retaining that capital internally for future reinvestment. As a result, the company’s share price will generally adjust downward by approximately the amount distributed.

For example, if a company is worth $100 per share and pays a $5 dividend, the share price will generally adjust to around $95 following the distribution. The investor has not necessarily created additional wealth - they have simply received a portion of the company’s existing value in cash form.

This is why sophisticated portfolio managers focus heavily on total return rather than dividend yield alone. Total return includes:

- Capital appreciation

- Dividend income

- Interest income

- Reinvested growth

Importantly, we remain strong proponents of high-quality cash-flow-generating assets such as infrastructure, real estate, private lending, and other real asset investments.

However, there is an important distinction between recurring cash flows generated by long-term contractual or income-producing assets, versus public companies distributing a portion of earnings that might otherwise have remained within the business for future growth.

While both approaches can provide investors with steady monthly or quarterly income, the long-term impact on the underlying asset, growth profile, and compounding potential can differ significantly over time.

High Dividend Yields Can Sometimes Be a Warning Sign

Another misconception is that a higher dividend yield automatically means a stronger or safer investment.

In many cases, the opposite can actually be true.

A stock yielding 8% or 9% is likely not yielding that amount because the company is thriving - it may simply be because the share price has fallen significantly due to deteriorating business fundamentals or investor concern.

This is particularly important in Canada, where many dividend-focused investors become heavily concentrated in sectors such as banks, pipelines, utilities, and telecommunications.

While these sectors can absolutely play an important role in portfolios, they are also generally more mature industries with slower growth profiles and greater sensitivity to factors such as interest rates, economic conditions, and regulatory pressure.

We have seen periods where high-yield companies experienced meaningful declines in share price while continuing to pay dividends temporarily - until eventually those dividends themselves were reduced.

It is important to remember that dividends are not guaranteed, and are only as strong as the underlying business supporting them.

The Reinvestment Tradeoff

One of the most overlooked aspects of dividend investing is what a company gives up when it distributes large portions of profits to shareholders.

Companies with strong growth opportunities often choose to allocate more capital toward future expansion rather than paying significant dividends, including:

- Expanding operations

- Acquiring competitors

- Developing technology

- Improving infrastructure

- Hiring talent

- Research and development

- Artificial intelligence and data initiatives

Historically, some of the strongest long-term performers globally paid little or no dividends during their highest-growth years because management believed those earnings could create greater value if deployed within the business.

A useful illustration of this concept can be seen when comparing mature dividend-paying companies against businesses that prioritized growth and capital reinvestment.

Over the past decade, Bell Canada (BCE) has remained a popular Canadian dividend-paying investment, known for its attractive dividend yield, which has often exceeded 5%. However, despite providing income to shareholders, and because the company's share price has declined significantly over the same period, investors experienced a negative total return over the past 10 years despite the dividend income received:

Source: https://www.financecharts.com/stocks/BCE/performance (May 29, 2026)

In contrast, Berkshire Hathaway, led by Warren Buffett, has famously never paid a dividend (source). Buffett has long argued that retained earnings can often create greater shareholder value when allocated to productive investments, acquisitions, and business expansion opportunities. Over the same period, Berkshire Hathaway generated substantially stronger capital appreciation and total shareholder returns.

Source: https://www.financecharts.com/stocks/BRK-A/performance (May 29, 2026)

Buffett is not alone in his belief that reinvesting in a business can create greater shareholder value over time. Many of the world's strongest long-term compounders generated exceptional shareholder returns by allocating capital internally rather than distributing a significant portion of earnings each year.

This does not suggest that dividend-paying companies are poor investments. Rather, it highlights the importance of evaluating investments through the lens of total return, growth potential, business fundamentals, and long-term capital allocation decisions rather than dividend yield alone.

The Canadian Tax Misconception

Canadian eligible dividends do receive favourable tax treatment through the dividend tax credit, which is one reason dividend investing remains especially popular domestically.

However, many investors overlook the flexibility advantages associated with capital gains.

Dividend income is taxable in the year it is received, regardless of whether the investor actually needs the cash flow at that time. Capital gains, on the other hand:

- Are taxed when realized

- Allow investors to defer taxation

- Currently result in only 50% of the gain being taxable in Canada

- Provide greater flexibility over when taxable income is generated

This distinction can be particularly important from a long-term planning perspective.

Consider an investor who owns a dividend-paying portfolio generating $10,000 annually in eligible dividend income. Even if the investor has no intention of spending those distributions and automatically reinvests the entire $10,000 back into the portfolio, the dividend income is still taxable in the year it is received. As a result, while the investment account may appear to show the full $10,000 was reinvested, the investor will ultimately owe additional tax when filing their return.

By contrast, an investor holding an appreciating asset that does not distribute significant income can defer taxation entirely until funds are actually required. During that period, the full value of the investment can continue compounding without creating an immediate tax obligation.

In addition, because only 50% of a capital gain is currently included in taxable income, capital gains can often result in a lower effective tax burden than other forms of investment income, particularly when combined with the ability to control the timing of realization.

For higher-income retirees, this flexibility can be especially valuable. Significant dividend income may increase taxable income each year and potentially contribute toward Old Age Security (OAS) claw back, regardless of whether the cash flow is needed. Investors holding appreciating assets with limited ongoing distributions often have greater control over when and how taxable income is generated.

This highlights the importance of considering not only how an investment generates returns, but also the tax implications and long-term planning opportunities associated with those returns.

Summary

In summary, we do not view dividend investing as inherently flawed, and dividend-paying companies can certainly play a role within a well-diversified portfolio. However, we believe it is essential to evaluate investments through a broader lens than dividend yield alone.

Ultimately, the true driver of long-term investment success is not simply the amount of income the portfolio may distribute, but the underlying quality of the businesses and assets being owned, their ability to compound capital over time, and how effectively the overall portfolio aligns with an investor’s financial goals, risk tolerance, tax considerations, and cash flow needs.

As such, our approach remains focused on diversification, strong business fundamentals, thoughtful capital allocation, and total return. This includes investing in a blend of traditional equities, real assets such as infrastructure and real estate, and other investments capable of generating both sustainable cash flow and long-term growth.

Rather than viewing dividends as the primary objective, we believe they should be considered one component within a broader, disciplined investment strategy designed to build long-term wealth, support retirement income needs, and provide financial peace of mind.

This publication is for informational purposes only and shall not be construed to constitute any form of advice. The views expressed are those of the author alone. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

- Hits: 687